Investing Beyond Credit Scoring to Strengthen the Loan Book

Introduction

Numida is a Y Combinator-backed digital SME lender operating across Kenya and Uganda. For nearly a decade, the company has invested heavily in credit scoring and operational systems to support responsible unsecured lending at scale.

As volumes grew, the team made a deliberate distinction. Credit models determine how much to lend based on the information presented. They are built to assess repayment risk at the individual level. They are not designed to surface coordinated activity across borrowers that can appear legitimate in isolation.

Fraud in digital lending is not limited to stolen identities or obvious misrepresentation. It can also include groups of borrowers applying in coordination, individuals accessing multiple loans through connected accounts, or patterns designed to increase total borrowing across a network. Some of these patterns may still repay initially, making them difficult to detect through repayment-based models alone.

To address that, Numida implemented Archer as a dedicated fraud control system, giving its risk team ownership over how coordinated patterns are detected and managed across markets.

Key Results at a Glance

Rules configured by Numida identified zero-payment defaults at more than 2x to 3x the baseline rate in Uganda backtesting.

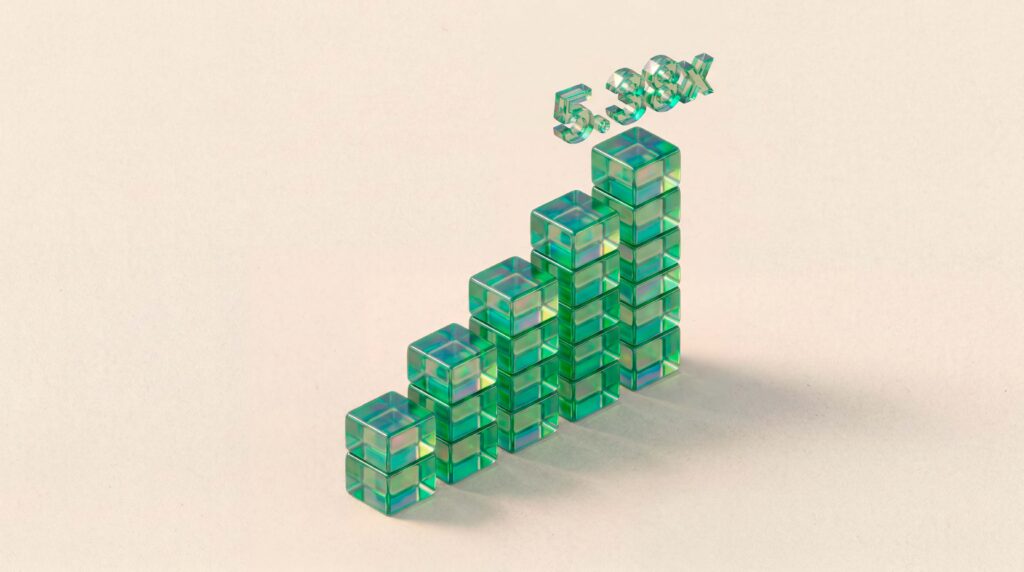

Approximately 5.38x net financial impact relative to subscription cost.

Fraud rules can be created or modified in under 60 seconds without engineering involvement.

Numida first deployed Archer in Kenya and later extended to Uganda after validating the patterns surfaced.

The Insight: Credit Risk vs Coordinated Behavior

Strong credit models are necessary, but they are not sufficient. They optimize lending decisions based on borrower-level data and repayment history. Coordinated behavior evolves differently from traditional credit risk signals and often sits outside that framework.

Numida chose not to assume that credit performance alone would surface these patterns. Instead, the company treated coordinated activity as a distinct risk discipline requiring its own control layer.

As Angus, who leads data at Numida, explains:

“We wanted visibility into patterns we might otherwise miss. Credit models are built to assess repayment risk at the individual level. They’re not designed to surface relationships between borrowers. Archer gives us that additional layer of visibility.”

The Operational Shift

Before Archer, adjustments to fraud rules required engineering cycles. Iteration depended on technical resources, which meant controls could lag behind borrower behavior.

With Archer, Numida’s risk team owns rule creation and management directly. Rules are monitored weekly and can be created or modified in under 60 seconds, without engineering involvement.

When a rule triggers, connected borrower activity can be reviewed immediately to validate whether a pattern reflects coordinated behavior. Controls evolve alongside what the team is observing on the ground.

Joyce, who leads risk for Numida, puts it simply:

“We review rule performance weekly and adjust directly in the platform. If we identify a new pattern, we don’t need to wait for engineering. That helps us keep our controls aligned with what we’re seeing on the ground.“

From Kenya to Uganda

Archer was first deployed within Numida’s Kenya operations. The initial objective was straightforward: give the risk team direct visibility into coordinated patterns that credit models were not designed to detect.

As rules were configured and monitored, the team began identifying repeatable patterns that were difficult to see within borrower-level decisioning alone. The signal was consistent enough that Numida chose to extend the same control layer into Uganda.

After validating the patterns surfaced in Kenya, Numida deployed Archer in Uganda to provide the same level of visibility and control across its larger, more established market. Rules were adapted between environments as borrower behavior differed, but the operating model remained the same: risk team ownership, immediate monitoring, and direct rule iteration without engineering dependency.

Results in Context

In Uganda backtesting, rules configured by Numida identified zero-payment defaults at more than 2x to 3x the baseline rate for the same cohort.

Under conservative assumptions, rules configured in Archer generate approximately 5.38x net financial impact relative to subscription cost.

More importantly, the impact was targeted. Rather than tightening credit across the board, Numida can isolate specific coordinated patterns while preserving approval rates for legitimate borrowers.

The result is not simply fewer loan defaults. It is greater control over how the loan book evolves as borrower behavior changes.

Why This Matters for Digital Lenders

Many digital lenders define fraud narrowly as stolen identities or clear misrepresentation. Coordinated borrower behavior often falls outside that definition, particularly when individual applications appear legitimate.

Strong credit models remain foundational. But as digital lending matures, separating credit decisioning from fraud control becomes a structural advantage.

Numida’s approach reflects that distinction. By layering dedicated fraud controls alongside its credit models, and giving its risk team direct ownership over those controls, the company strengthened its loan book without slowing operations or overcorrecting on approvals.

For lenders who believe their credit systems capture all relevant risk, the question is not whether the models are sophisticated. It is whether they are designed to detect coordinated activity across borrowers in the first place.